In this week’s guest member blog post, we hear from Gil Sadeh, President of Kenshoo Skai who shares how publishers and retailers can thrive within and across walled gardens. He reveals how to successfully navigate the complexities of modern digital advertising and scale growth, beyond offering inventory with rudimentary demand levers.

Advertising operates within a cycle driven by the basic economic principles of supply and demand. Publishers provide ad inventory, and advertisers invest in these platforms based on their effectiveness in driving consumer engagement and transactions. This demand for ad space perpetuates the cycle, particularly in digital walled gardens like Amazon, Google, and Facebook, where targeted consumer engagement meets sophisticated ad-delivery mechanisms.

As the digital ecosystem grows more complex, simply participating in this cycle is no longer adequate. Publishers and retailers must adopt advanced strategies to grow demand effectively within their gardens, evolving to help advertisers leverage these complexities to their advantage.

Build it and They Will Come?

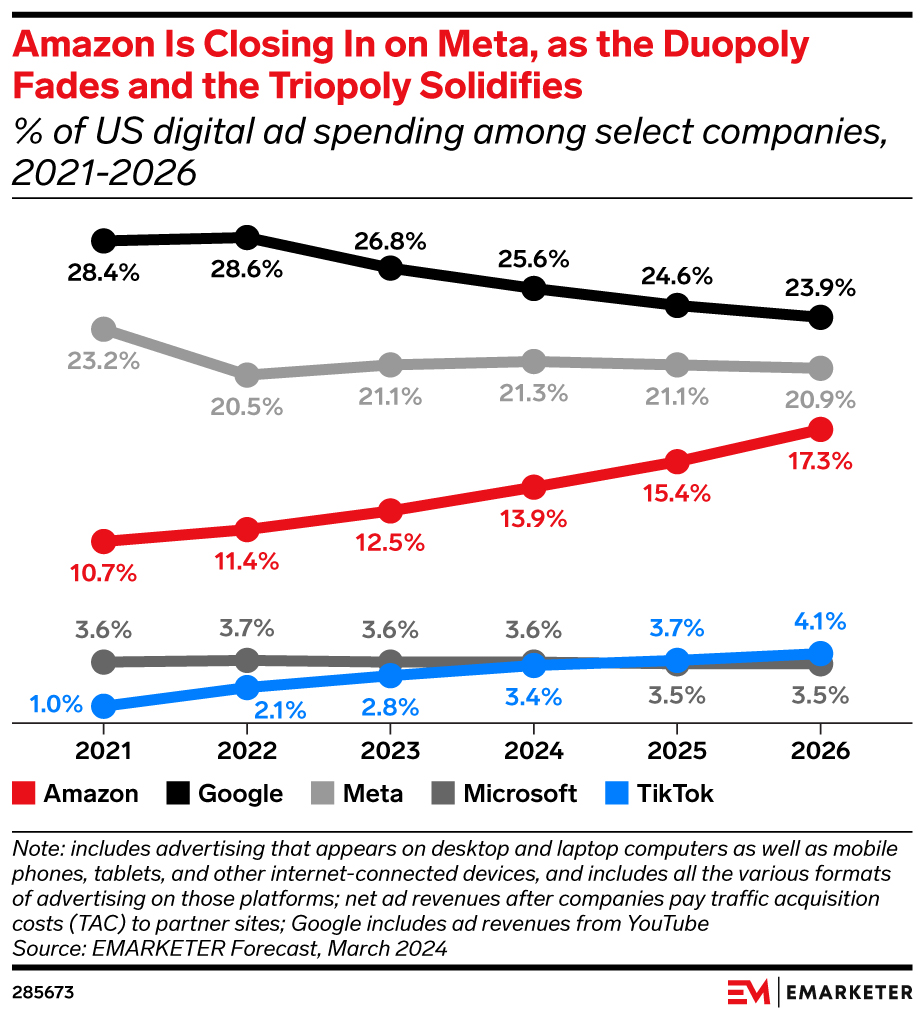

Platforms like Amazon, Google, and Facebook, with their billions of monthly active users, have attracted massive advertiser demand. With over 50% of all online audiences now in cookieless environments, the reliance on first-party data makes these platforms particularly attractive for advertisers. The ‘big three’ account for over 60% of all digital ad spending — a number that continues to rise.

As ad budgets increasingly favour walled gardens, the supply side has experienced a renaissance. According to eMarketer, over 200 Retail Media Networks (RMNs) have been launched worldwide as of August 2024. New social platforms have joined the scene, and even non-traditional sectors (finance, travel, telco, delivery, etc.) are creating their own media networks, such as Chase, United Airlines, T-Mobile, Uber, and more.

But opening up supply isn’t enough. While initial novelty and access to new audiences brought with it advertiser budgets and quick wins for retailers, this advantage is fleeting. Many networks are already struggling to hit fill rates and maintain advertiser interest. With hundreds of competitors now in the field, the focus must shift from building and connecting supply to effectively growing and scaling demand.

The true challenge now lies in not just attracting advertiser interest, but also continuously enhancing the value provided. As the market matures, scaling demand requires incorporating advanced demand-capture capabilities and ongoing optimisation. Advertisers are increasingly sophisticated, seeking to use first-party data to create highly targeted campaigns and gain deeper insights into consumer behaviour. Therefore, platforms must evolve beyond offering basic ad space to deliver innovative solutions and advanced tools that meet these elevated expectations.

Looking Towards the Future: Data-Driven Demand Strategies

To successfully navigate the complexities of modern digital advertising and scale growth, platforms must go beyond offering inventory with rudimentary demand levers. Here are five key areas of focus:

1. Unification of Supply and Demand: This will streamline operations and drive sustainable growth by creating a more cohesive and efficient platform for managing media investments. Retailers must work towards providing seamless experiences where advertisers can easily access and optimise their campaigns across multiple touchpoints.

2. Omnichannel Integration: The expansion of retail media into commerce media and the formation of partnerships between walled gardens highlight the need for a robust omnichannel approach to enhance engagement and impact. This will allow advertisers to effectively reach consumers wherever they can be found while ensuring that marketing efforts are synchronised and effective, leading to better ROI.

3. Advanced Analytics and Insights: By leveraging comprehensive data beyond traditional ad metrics, these platforms will enable more effective optimisation and transparency, helping advertisers understand the true incremental value of their campaigns. Predictive analytics, machine learning, and AI will play pivotal roles in personalising content to drive higher engagement rates.

4. Enhanced Targeting and Personalisation: Platforms must utilise first-party data to create highly targeted campaigns that resonate with specific audience segments. By offering granular audience targeting options and dynamic creative optimisation, platforms can help advertisers achieve greater precision and relevance in their messaging.

5. Advanced Planning and Forecasting: While optimisation is often associated with managing ongoing campaigns, its application in campaign planning is equally vital for mastering demand in digital advertising. Integrating AI into campaign planning will streamline the process, enhance targeting accuracy, and better forecast demand shifts. This ensures that advertising strategies are proactive and responsive to market dynamics.

The New Currency

Clearly, the future of digital advertising is demand. But to realise that future, retailers, and publishers must act quickly to innovate and implement advanced, data-driven strategies in the present. Long-term success requires being able to span both walled gardens and the open web while removing complexity from these high-yield environments.

With the right solution, the better-positioned platforms will be able to capitalise on their investments to unlock and harness scaled and diversified ad demand across the multiple consumer touchpoints of commerce media.

On the 10th and 11th July, representatives from more than 10 Retail Media networks in Europe gathered to discuss and debate in-store Retail Media. As Retail Media continues to grow and evolve, more channels and formats become key to the overall media mix. IAB Europe wants to ensure standardisation is in place across all Retail Media channels, including in-store.

Key takeaways of the Workshop include:

In April, we published measurement standards for on-site and off-site Retail Media ads. We convened this second workshop in Paris, supported by Criteo, to ensure there is consistency in how in-store Retail Media is defined and the measurement standards applied to those formats. We are working in parallel with IAB US to develop consistent standards across Europe and the US. It is worth noting that Europe is 3 to 5 years ahead of North America in the development of in-store Retail Media. This is particularly evident when comparing the shopping experience of a typical American supermarket with European stores.

The Retail Media networks represented at the Workshop were:

Thanks to the support of Criteo for hosting the Workshop at their offices, we enjoyed two days of rich discussion, debate, and alignment on in-store Retail Media standards in the areas of in-store ad formats, store zones, media metrics and sales measurement. The Workshop was moderated by Yara Daher and Marie-Clare Puffett and featured insights from industry analyst, Andrew Lipsman, RMNs Ahold Delhaize and SMG. Advertima and Venvee also collaborated with IAB Europe on the development of the content for the Workshop. Discover what was discussed below.

Day One

The Workshop kicked off with a discussion around the definition of in-store Retail Media and the formats that are in scope. The group broke out into pairs to discuss whether in-store should be defined as digital or measurable.

The group was then joined by Andrew Lipsman for industry insights and thought-leadership on the development of in-store Retail Media. Key takeaways from Andrew’s presentation include:

The group was also joined by Ahold Delhaize and PRN for an in-store case study and measurement overview. The workshop then moved onto the topic of media measurement and how an ad impression and opportunity to see can be defined in a store environment. The group took inspiration from the MRC Digital OOH Measurement Guidelines. The group managed to align on a framework for defining an ad play, ad impression, opportunity to see and likelihood to see.

The end of day one concluded with a session on store zones and how these can be defined and the type of executions included within each zone.

Day Two

Day two kicked off with a networking breakfast followed by a summary of the previous day. The group doubled down on finalising a definition for in-store Retail Media and the associated groups of ad formats followed by a final discussion on defining ad plays, impressions and opportunity to see. The group then focused on sales measurement and discussed what the key metric and attribution window for in-store sales is. The group agreed that sales / brand lift is key to the measurement of in-store media as well as incremental sales lift. The group also discussed the different approaches to measuring these metrics, e.g. A/B testing, multivariate testing and one to one vie technology solutions.

Commenting on the workshop, Jessica Wegner, Senior Vice President of Retail Media at DOUGLAS said: “In-store Retail Media has the potential to disrupt advertising, whether it is capturing media budgets from linear tv or challenging DOOH. Transparency around calculations and standard definitions to KPIs is key to the product’s entry into the programmatic advertising ecosystem, which will unlock its scalability to compete with onsite and offsite retail media. Douglas Marketing Solutions is happy to play a pioneering role in moving this needle forward via the IAB Europe standardisation initiatives.”

Summary

Overall, the Workshop is a pivotal moment and a key starting point for the industry to define in-store Retail Media and the associated measurement metrics.

The outcome of the workshop will be an initial set of recommended standards for in-store Retail Media metrics and measurement. A document outlining the recommendations will be published as an initial draft for industry feedback within the next month.

The development of Standards for Retail Media Advertising in Europe is a key focus of the IAB Europe Retail Media Committee work plan. This multi-stakeholder Committee brings together retailers alongside leading Retail Media businesses in Europe to advance and shape the future of this exciting digital advertising space and has already produced valuable resources including pan-European definitions, the first-ever industry association-led Retailer Digital Advertising Capability Map a Retail Media Glossary. You can find all of these resources and more on IAB Europe’s Retail Media Hub here.

To find out more about IAB Europe’s Retail Media work and how you can get involved please contact IAB Europe’s Industry Development & Insights Director, Marie-Clare Puffett.

In this week's member guest blog post, we hear from Maurits Priem, VP Monetisation Europe & Indonesia at Ahold Delhaize as he reflects on Cannes Lions and shares his 7 key takeaways on Retail Media. Is Retail Media here to stay? Find out below.

Last month, the Cannes Lions Festival brought the global media industry together in the South of France. One of the trending topics at the event was Retail Media, as it is revolutionising the way brands can reach customers. This article discusses the key takeaways on Retail Media, coming directly from Cannes Lions 2024.

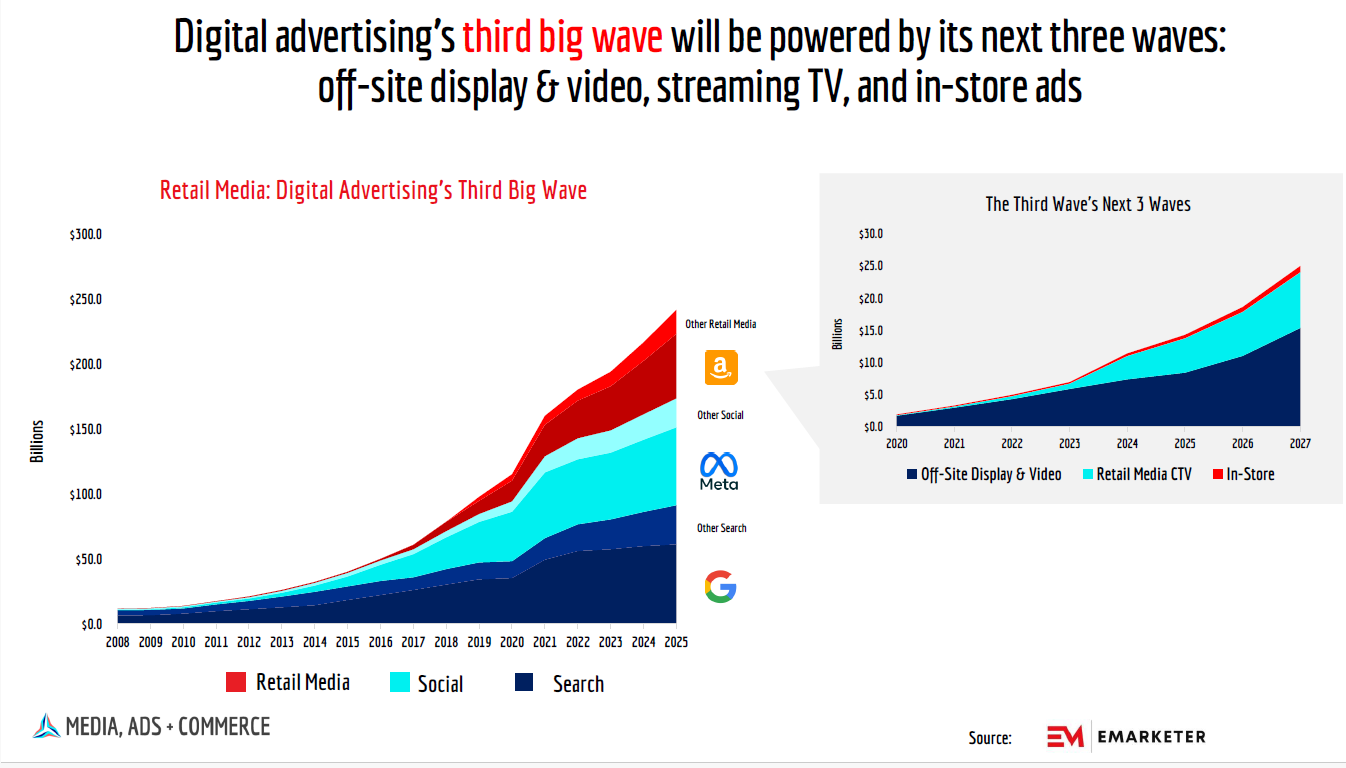

CMOs incorporate Retail Media in their omnichannel marketing and retailers grow and mature their Retail Media networks (RMNs). Both at a remarkable pace, dubbed ‘The Third Wave’ of digital advertising. This year, Retail Media will already make up one-fifth of worldwide digital ad spend.

At the Cannes Lions Festival, retailers, advertisers, agencies, ad-tech and industry bodies met to learn more about this dynamic development, as well as to professionalise, network, and negotiate. This year, we counted over three times more events, panels and talks on Retail Media compared to last year. We estimated a similar increase in retailer’s attendance, which led to the rather unique opportunity to discuss Retail Media in person with players from both sides of the Atlantic. Clearly, Retail Media is in Cannes to stay.

Retail Media is projected to grow beyond this year’s $140B globally at a continued pace of 20% annually. In essence, advertising is about reach, data (targeting & measurement), technology (enabling & convenience) and creativity. Retail Media’s growth will be driven by scaling the first three axis. Building significant scale in terms of reach, data and tech demands for vast resources in terms of talent and budget. Most likely, only large omnichannel retailers are equipped to qualify for that game. At the same time, advertiser’s demand will look for efficiency and work with just one or two RMNs to meet sufficient reach in a given geography and then move on to the next region. Therefore, growth will probably go hand in hand with consolidation and aggregation. Winners will take all.

Nevertheless, smaller RMNs may still maintain their business based on the joint business plans (JBPs) in trade relations with their suppliers/advertisers. For an advertiser this fragmentation leads to inefficiencies, consistency challenges, and reluctance to spend media budgets, all probably hindering growth at the speed of the large omnichannel RMNs.

Retail Media is very different from retail. Depending on the country, the number one selling grocery item may well be a banana. However, selling a banana is very different from selling a banana ad campaign. The supplier-buyer relation flips 180 degrees; the focus is on technology and scalability rather than food and logistics. It is a high margin instead of a low margin game. Thus, in order to create the anticipated growth, to be able to surf the ‘Third Wave’, there is much to learn, for retailers as well as for advertisers.

Retailers need to be committed to build this new capability, and advertisers need to be committed to work full funnel and omnichannel. Today, budgets, KPIs, data and expertise are still way too siloed. There is a change management challenge at both sides of the table and in order to cross this chasm, retailers and advertisers should collaborate. It’s time to take joint surfing lessons.

Targeting of key audiences becomes more and more sophisticated with retailer customer data platform (CDP) adoption and integration into self-service platforms. Multiple RMNs announced self-service and programmatic solutions at Cannes, bringing convenience to advertisers and their agencies, soon to become a hygiene factor.

RMNs in the United States seem to have discovered physical stores as the next frontier. In their rush for gold they realise that many European RMNs are rooted in their stores, therefore they are looking for European learnings and connected store developments. The challenge is to unlock the truly unique value that physical stores can add to online and vice versa. Omnichannel connections and integration demand for cross-silo collaboration; instore budgets, KPIs, data and expertise are often sitting in silos, like retailer store development, advertiser’s field force and shopper marketing. The European and American IABs hosted a first of its kind transatlantic workshop on in-store industry standards, recognising the advertisers need to avoid a patchwork of walled RMN gardens, each having their own metrics, formats and definitions.

In other RM topics (except for privacy) the USA Retail Media industry is clearly ahead of Europe, just like Asian Retail Media in turn is most mature globally.

Offsite advertising, in which Retail Media leverages its unique customer insights, continues to take shape, providing an opportunity to advertise through large publishers and social media networks. Amid crumbling cookies, retailers hold large sources of consented first-party data. Data on audiences that can be tested, confirmed and augmented against each purchase at a SKU level. During the festival, multiple RMNs announced offsite products, driving reach for their advertisers.

Like any booming industry, Retail Media attracts new entrants joining the party. As predicted some years ago, other commerce, like airlines and fitness companies, stand up their own RMNs, some of them present in Cannes. Given their small endemic supplier base, these new RMNs serve near-endemic and non-endemic advertisers mainly.

We see a growing appetite from these non-endemic brands to advertise through RMNs. Both offsite as well as onsite. These non endemic advertisers are attracted by RMN’s additional and unique reach and its first-party audiences (not just search and likes, but actual buying behaviour) to mitigate looming cookie depreciation. In addition advertisers are attracted by its brand safe context, the possibility to reach consumers in buying mode (higher attention, more open to ads and longer dwell times) and last but not least the opportunity to stand out as a non-endemic brand in a retail context (Seth Godin’s ‘purple cow’).

Huh, No AI?!

Of course, AI was a topic as well. But less hyped than last year. With numerous Retail Media AI initiatives being launched at Cannes, the short-term effects might easily be overestimated, as with many innovations. The long-term effects, however, are deemed to be huge. AI’s game-changing potential is to be found in use cases such as media planning, campaign workflows, creative versioning, performance optimisation and next-level targeting.

Conspicuously Absent Retail Media Topics

We may have missed it, but there was little to no talk on the consumer perspective, in the Retail Media business bubble. Whilst there is abundant opportunity for RMNs to improve consumer experience. For users, a good experience means fewer irrelevant ads, fewer third parties recklessly tracking and sharing personal data, and less redundant clickbait.

Finally, we missed ambitions on the role of Retail Media in Environmental Social Governance (ESG). We see ample opportunity to raise the bar in advertising in terms of relevance (for consumers and advertisers), carbon emissions, privacy, and amplifying good products and messages.

Surf’s up!

Retail Media is in Cannes to stay. We hope to see you there next year. Till then, let’s continue to take joint surfing lessons, learning to ride ‘The Third Wave’.

In this week's member guest blog post, we hear from Pete Danks, VP of Market Activation at Magnite & Lead of IAB Europe's Post Third-Party Cookie Working Group. He discusses if confidence really is eroding as the cookie crumbles. Pete takes a look at the work IAB Europe’s working group is doing and our findings from recent research into this topic to share his view on whether the market is ready.

As reported by Digiday, recent research by Adobe suggests a troubling trend. Their study indicates a decrease in marketer confidence regarding the post-cookie landscape. In 2022, the majority (78%) of marketers felt prepared for the cookie's demise. By 2024, that number had dropped almost a quarter to 60%.

Put another way: as we get closer to the potential beginning of the end, reality seems to be kicking in.

At IAB Europe we run a working group on this very topic, which brings a mix of sellers, buyers, and technology vendors together from across Europe and further afield. In February we published the following study: The Post Third-Party Cookie Countdown: Industry Readiness and it is interesting to see how things are evolving.

Indeed we have seen this backward trend is somewhat mirrored in our own findings. At the recent IAB Europe Interact conference in Milan, we posed the same question from the survey to the live audience: "Do You Agree That You/Your Company Is Prepared For The Deprecation of Third-Party Cookies?"

This time, only 21% of respondents strongly agreed - a decline from nearly 31% earlier this year.

Factors Influencing the Confidence Crisis

Our original research revealed some key factors stopping respondents from feeling confident about their readiness including;

1. A lack of Strong First-Party Data Strategies

2. Needing more Industry Collaboration and Standards

3. Needing more Education and Communication

4. Driving Innovation and Solutions Beyond Cookies

Perhaps the confidence scores suggest that the industry hasn’t made enough progress in these areas.

A Closer Look: Pragmatism Beats Optimism?

While confidence may be waning a little, it's important to note that it hasn't disappeared.

Over 50% of respondents who participated in our poll at Interact still agreed or strongly agreed with the statement about being prepared. This is an almost identical figure from the February survey - it’s a noticeable shift from strong confidence to a more hesitant or neutral position.

Our Interact audience data showed a full third (33%) expressed neutrality, which is a significant increase from 16% earlier in the year.

This may indicate a transition from a proactive, ready-for-change mindset to one of uncertainty and cautious optimism.

Why does it Matter and How can we Help?

Away from the largest players in the online advertising space, this stuff really matters. What many of us call the “Open internet” is far more exposed to cookie deprecation, data erosion and privacy legislation. And for perhaps the first time, the quiet bit has been said out loud;

That is a call-to-arms for anyone that isn’t a ‘walled garden’ to take action. SSPs like Magnite for example are working hard to help aggregate small and medium publishers in meaningful ways, and allow for first party data activation at scale. In the IAB Europe working group, we are exploring multiple solutions as part of the education and innovation challenges called out earlier in this post. Ultimately, it feels like now is the time to work together with peers, partners and even competitors if we want to tackle these challenges robustly.

**IAB Europe’s Post Third-Party Cookie Working Group has been formed to help foster a collaborative and informed community in anticipation of the imminent removal of third-party cookies. The working group’s mission is to empower stakeholders from across the digital advertising ecosystem with the knowledge, resources, and support necessary to navigate the evolving landscape. To join please contact Helen Mussard

In this week's member guest blog post, we hear from Nick Clegg, President, Global Affairs at Meta. Former Deputy Prime Minister of the United Kingdom, leader of the Liberal Democrats, member of Parliament, to discuss the European elections and what this means for Europe’s economy. He discusses the opportunities that now present themselves to Europe and how we can change the course.

The people of Europe have voted. A new parliament has been elected. The runners and riders for the European Commission President and the new slate of Commissioners are jockeying for position. Some old hands could be coming back; some young guns are hoping to make their mark. But this is not business as usual for Brussels.

No matter who ends up in the seats when the music stops, the task they will inherit is existential. Thirty years ago, Europe represented roughly a quarter of global GDP. Now we’ve fallen behind. GDP per capita in the EU is half of that in the US, at approximately $40,000 per European compared to $80,000 per American. None of the world’s top 10 companies are European. None of the dozen most valuable unicorns — startups valued at $1 billion or more — are European. Of the Top 50 companies in Europe none of them were founded within the last 30 years.

Our companies are growing more slowly, reporting lower returns and lagging behind their peers in research and development, even in industries that were traditionally Europe’s strength like automotive and manufacturing. Just one of the top ten electric vehicle brands in the US last year was European. There are four times more semiconductor plants planned in China than in Europe.

The sad fact is the EU is no longer a fertile ground for innovation and world-class companies. As Emmanuel Macron and Olaf Scholz have stated starkly: “Our Europe is mortal”. In their words, Europe is experiencing its “Zeitenwende” — an historic turning point. But which way it turns remains to be seen.

The era of generative AI presents an opportunity to change the story. These powerful technologies could provide a massive boost when we need it most. Goldman Sachs estimates that generative AI could increase global GDP by seven per cent over the next decade.

Europe is a pioneer of tech regulation — as GDPR, the DMA, DSA and AI Act demonstrate — but not yet at pioneering and deploying the tech at scale itself. Europe’s regulatory complexity and the patchwork of laws across different member states often makes companies hesitant to roll out new products here. Meta, Google and others have delayed rolling out their AI assistants here, and even European success stories like Volkswagen are increasingly leaving to build and launch their AI products in the US. With the rapid adoption of AI in the US and China, the gap between these superpowers and the EU is widening.

How can Europe change its course? The underlying infrastructure for foundational AI models is hugely expensive and energy-intensive. But deploying and customising AI models, especially open source ones, will give European businesses, start-ups and researchers access to tools they wouldn’t otherwise be able to develop on their own. With Europe’s high quality university sector producing top talent, and our deep capacity for research and development, we could become a world leader in the application layer of AI — creating the apps and services through which people experience this powerful new technology.

Europe isn’t playing to its biggest strength — its single market of 450 million consumers. European leaders have stated repeatedly that one of their main goals is for Europe to compete with the US and China in tech. They long for the next Silicon Valley to emerge on European soil. I share that ambition. As a proud European, I would love to see the next Meta, Alibaba or Google emerge on the continent. And we have all the necessary ingredients: a vast consumer market, great universities, top talent, and a history of experimentation and innovation.

But for all the regulatory activism — a staggering 77 new pieces of EU digital legislation have been adopted since 2019 — we have been held back by our failure to properly complete the digital single market. It is striking, for instance, that a digital startup in Amsterdam would still have to navigate 27 different intellectual property laws, various rules for the licensing of content, data protection authorities and other obstacles before it could go live across the continent.

During my years in Brussels as a young man in the 1990s, the single market was cause for huge optimism. I studied at the College of Europe — where I met my wife Miriam — and became an official in the Commission during the heyday of globalisation and European integration. The Berlin Wall had fallen, the Single European Act was bedding in, the Maastricht Treaty was hot off the presses and the WTO was up and running. I was then an MEP in the late 1990s and early 2000s, when it felt like the world was growing closer together and the EU — this remarkable experiment in cooperation, openness and strength in numbers — was the symbol of that optimism.

That feels like a long time ago now. The 2008 financial crisis broke the back of globalisation. A cloud of introspection fell over Europe as governments, loaded with huge deficits and enraptured by anti-establishment populists on the left and right, prioritised issues of national sovereignty over shared endeavour. No country turned its back on the European project more emphatically than my own country, the United Kingdom. The architects of the single market — not least its British mastermind Lord Cockfield — would be spinning in their graves if they saw how it just isn’t delivering the prosperity Europeans need today. Instead, the EU is increasingly disputatious and fragmented, with regulators and policymakers pulling in different directions. It’s little wonder so many voters, especially young people, are supporting insurgent populists promising to shake up the status quo.

I believe we can get that optimism back. Our new Parliamentarians and Commissioners face a huge task to reverse Europe’s economic decline. It won’t be easy but it is possible. We just need to play to our strengths. The single market is Europe’s biggest asset but it isn’t complete. Finish the job. Avoid fragmented regulation. Embrace an open approach to AI development. Then let European creativity, ingenuity and entrepreneurialism bring back the optimism we all crave.

Three months after the entry into force of the Digital Services Acts, IAB Europe and IAB Tech Lab would like to understand how industry players are leveraging the DSA Transparency OpenRTB extension intended to facilitate compliance with Article 26, which issues they may be experiencing, and where they need more support. Your valuable input will only take a few minutes to share and will be kept strictly confidential.

The survey is open for your participation until Friday 28th June 2024.

On 21-22 May we hosted our annual flagship conference Interact 2024 in Milan where we brought over 240 industry leaders, innovators, and experts together to answer the big questions needed to shape the future of the digital advertising and marketing industry.

Thanks to the support of our sponsors, media partners, the team at IAB Italy, and our event host Joanna Burton, we enjoyed two days of content, which focused on our theme ‘The Big Questions. The Smart Answers’.

Going beyond standard keynote presentations and panel discussions, we brought the ‘interactive’ back to Interact this year, with each session framed around a key question that our elite, expert speakers endeavoured to answer. No beating around the bush. It was all about delivering smart answers to the industry's most important questions. Plus we addressed additional questions live on stage through our engaging polls and audience Q&As.

On day one, we focused our attention on tackling the industry’s biggest challenges and innovations head-on, exploring key topics and unearthing the much-needed answers to areas including the latest digital ad spend figures, what buyers want from digital advertising, how ready the industry is for a world without cookies, what’s next for programmatic TV and Retail Media and if we are measuring the right things.

Below you can find overviews and key takeaways from each session.

Interact 2024 opened with a keynote from our Chief Economist, Daniel Knapp, revealing the top-level results from IAB Europe’s widely-anticipated 2023 AdEx Benchmark Report to show whether the digital advertising industry experienced growth for 2023 and if so, what markets and channels contributed to this growth.

Daniel gave an exclusive presentation on the key results which will be released on the 12th June! Mark this date in your calendars to access IAB Europe’s 2023 AdEx Benchmark Report. This is the definitive guide to digital advertising expenditure in Europe.

Following the opening keynote, to ensure we deliver on the growth seen and that we have all of the y components in place to attract advertiser investment, key speakers from Diageo and TIM Group joined the stage to reveal the secrets of what they are really looking for when it comes to digital advertising. They shared exclusive priorities and focus areas, innovative areas that excite them, and their thoughts on what they think is driving the future of digital advertising.

Speakers:

Key takeaways:

Continuing on the theme of asking questions to the buy-side, our next session explored the evolving relationship between creativity and technology in content creation with speakers delving into how agencies harness emerging technologies to push the boundaries of storytelling and brand communication. From immersive experiences to AI-driven content, the group answered questions on the latest trends, challenges, and opportunities in leveraging technology to enhance creativity.

Speakers:

Key takeaways:

Next, it was time to tackle one of the industry’s most discussed topics of 2024 - the post third-party cookie era. Given the importance of the subject, the next few sessions were dedicated to answering key questions about how stakeholders are preparing to navigate this new paradigm.

To kick off the cookie conversation, Mediaplus argued that the abolition of cookies is not imminent but has already happened. With alternative targeting technologies already established, they revealed how data minimsation makes advertising better, not weaker.

Speakers:

Key takeaways:

In the next session, Google and Adlook joined the conversation to discuss how future-thinking ecosystem players are preparing for third-party cookie deprecation. Covering innovative solutions based on Privacy Sandbox technologies they explored what actions you can take today to get ready and stay ahead in the post-cookie world.

Speakers:

Key takeaways:

To further explore and round up the conversation on the impending world without cookies, our next panel answered key questions on the current challenges, opportunities, and strategies for navigating the post-cookie era, assessing whether our industry is ready for this seismic shift and how strategies can be adapted to ensure effectiveness in the future.

Speakers:

Key takeaways:

With the post third-party cookie questions answered, it was time to turn to outcomes and other challenges marketers face. In a world affected by the pandemic, climate crises, and misinformation, there are multiple challenges for marketers to overcome. In this keynote, IAS shared strategies for combating misinformation, safeguarding brand reputation, and fostering consumer trust. They also discussed the importance of adopting tools to face ever-evolving circumstances.

Speaker:

Key takeaways:

It was then time to turn our attention to one of the industry’s most discussed and rapidly evolving channels - CTV and addressable television. With so many questions, panels, podcasts and conferences on this topic, we wanted to give it due care and attention by starting with a fascinating keynote from RTL Group. Focusing on the recently announced tech cooperation between RTL Deutschland and ProSiebenSat1, RTL explored what it can do, how it opens up completely new performance dimensions in total video advertising for publishers, agencies, and advertisers, and what the future holds.

Speaker:

Key takeaways:

To explore the wonderful world of TV further, our next session brought industry leaders together to address the rise of TV programmatic buying in Europe. To answer questions on how it’s growing and what will happen next, the panel explored the challenges and opportunities inherent in this evolving and often complex landscape and shared insights and practical examples of how TV buying is moving to the mainstream.

Speakers:

Key takeaways:

It was then time to move on to another high-growth channel - Retail Media. Much like CTV, Retail Media has captivated investors, journalists, and buyers in 2024. During this session, speakers teased out the answers to the much-asked questions on Retail Media. Reflecting on the current state of Retail Media in Europe and its future trajectory in digital advertising, they explored the hurdles we need to overcome to fuel growth and innovation and the key opportunities retailers as media businesses present to brands.

Speakers:

Key takeaways:

To round up the day we turned our attention to measurement. Welcoming Brand Metrics to the stage and setting the scene on measurement, this keynote explored the changing nature of campaign outcome data in shaping future strategies by drawing exclusive insights from 30k+ brand lift measurements. .

Speaker:

Key takeaways:

And just like that, we were at the end of day one, and what better way to finish the day than by answering some of the arguable most important questions on measurement? To round everything up and leave our audience with the answers to what tools they should be using, panelists in the last session explored whether we are measuring the right things and what our focus should be on in terms of measurement as we move into a new era of digital advertising.

Speakers:

Key takeaways:

After a jam-packed day of interactive and engaging content, attendees were invited to attend a networking cocktail reception to continue the great conversations and connections, and to celebrate with fellow attendees.

Check out the Day Two highlights here.

From 6-9 June, EU citizens will be voting for their 720 representatives in the Parliament. To help navigate the upcoming changes and challenges, we have provided a brief overview and analysis of important aspects surrounding this year’s elections below.

Political Landscape:

According to the current political climate, the next European Parliament is expected to witness a significant increase in its centre-right and right-wing seats. Currently, the biggest parties in the European Parliament are the European People’s Party (EPP; centre-right, currently 179 seats) and the Progressive Alliance of Socialists and Democrats (S&D; centre-left, currently 141 seats). The third biggest party is Renew (currently 101 seats), which has a complex membership of mostly centre parties, including centre-left, centre-right and liberal factions. The Greens (centre-left, left-wing) slightly outweigh the European Conservatives and Reformists Party (ECR; right-wing). However, recent polls indicate that the rise of right-wing parties and sentiments in Europe may change this dynamic.

Although the EPP and S&D will likely remain the largest parties in the Parliament, the ECR (predicted 1 to obtain 72 seats ) and ID (Identity and Democracy, predicted to secure 66 seats) are likely to experience an increase in votes, while the Greens are expected to see a decline in support (predicted to secure 41 seats). This shift could influence future coalition-building, voting behaviour, and the Parliament’s own initiatives.

Despite many parties, including the Socialists, Greens, Renew, and Left parliamentary groups, signing a declaration calling upon all democratic parties to reject coalition-building or any alliances with the far-right , the EPP has refused to sign the declaration. Multiple national parties have signed agreements with far-right parties in their countries, such as the Renew equivalent (VVD) in the Netherlands. This is an important factor since the EPP will remain the largest party in the Parliament and could cooperate with the right-wing (ECR) and the far-right (ID) to secure a majority on new or ongoing legislation. This cooperation could support more "business-friendly" policies.

Key Issues:

Several key issues and pieces of legislation will shape the next mandate and be important to the digital advertising industry. For instance, the upcoming review of the GDPR will be a significant part of the next mandate. Although there is a general reluctance among policymakers to reopen the GDPR debate, there could be important changes or additions that impact the industry. IAB Europe submitted in January 2024 its feedback to the public consultation on the GDPR to represent members’ experiences, successes, and grievances with the law's application.

Another important aspect of the next mandate will be the implementation and enforcement of newly introduced legislation, namely the DSA, DMA, and the AI Act. Policymakers and the digital advertising industry alike are calling for the next Commission to invest time and resources into the efficient and harmonised enforcement and implementation of these regulations.

Additionally, the upcoming report on the Digital Fairness Fitness Check, an initiative launched in 2022 by the Commission to evaluate existing consumer legislation, will provide insights into whether these laws ensure an adequate level of consumer protection in the digital environment. This report will address issues such as dark patterns, personalization practices, and influencer marketing. Expected to be published in June, the report will also include main outcomes from the cookie pledge initiative.

Furthermore, rumours indicate that the Commission is likely to revisit the ePrivacy regulation in the next mandate. The pending proposal, which has been on hold for years already, will most likely be withdrawn and might come back in a different shape with a new proposal or multiple new proposals tackling different provisions within the ePrivacy directive.

Candidate Profiles:

The ‘Spitzenkandidaten’ procedure requires all political parties to nominate a candidate for the position of the Commission President. The following candidates have been nominated for the position:

Many expect Ursula von der Leyen to remain in her post due to the predicted prominence of the EPP in the European Parliament. However, this remains to be seen, as the Commission President has to be approved by the Parliament by an absolute majority. Ms von der Leyen remaining in power could mean that the next Commission increases focus on the implementation and enforcement of the legislation introduced during the previous term. Other important personalities and posts to mention include Didier Reynders, the former European Commissioner for Justice, who has taken unpaid leave from his position to be a candidate for the position of Secretary General at the Council of Europe.

Timeline after elections:

As the elections are drawing near, here are some important key dates following the elections that will shape the EU’s next mandate’s trajectory.

1 Polls conducted by Politico & Euractiv.

In this week's guest member blog post we caught up with Frazer Locke, Director, EU & APAC AdTech Sales at Amazon Ads. In this blog he looks at improving relevancy through model-based solutions, building better connections with context-based insights and empowering brands with clean rooms. For more on how brands can move beyond third-party cookies, keep reading.

Let’s be honest, third-party cookies have always been limiting. Despite being widely used they offer a false precision, and the continued conversation around what marketers will do when they’re deprecated remains a distraction. Now is our chance to do better, for both consumers and brands.

The way we can help brands to do better, and deliver relevant advertising that matches customers with products and brands they’re genuinely interested in, is through solutions such as audience modelling and contextual targeting. These solutions are powered by a combination of contextual and first party signals using advanced AI, to deliver advertising that is more relevant and helps brands better understand how their customers shop, stream, and browse. They will define the next era of digital advertising, and brands can start their journey today, by utilising solutions that are already available, all without a third-party cookie. Here’s how:

Improving relevancy through model-based solutions

86%₁ of consumers now consider the experience a company provides to be as important as its products, placing an even greater emphasis on brands to deliver relevant, interesting advertising. Model-based solutions can use shopping, contextual signals and purchase signals to predict ad relevance to help customers discover new products and brands while they browse online.

Powered by AI and machine learning, modelled solutions get smarter with every campaign that runs, improving engagement for the future. This increased relevancy can have a big impact. For example, we’ve seen brands across verticals experience a 34.1% 2 increase in return on ad spend, without having to take any action, after utilising our modelled solutions.

Building better connections with context-based insights

We know addressability remains a key priority for brands, and that this will only be compounded as 95% 3 of web traffic is expected to be unaddressable via traditional advertising methods by the end of this year.

Using AdTech to unlock real-time content consumption insights already available to brands today is an obvious place to start. For example, contextual targeting helps brands reach consumers based on current content consumption, without relying on ad IDs. It does this by enabling brands to select the specific products, categories, and content where they want their ads shown. This helps brands engage with audiences who are already in a mindset aligned with the content they're consuming.

At Amazon Ads we take this a significant step further. When brands use the Amazon DSP, we use AI and AWS models that leverage our shopping, streaming, and browsing signals with metadata about the content being viewed (i.e., contextual signals) to better ensure customers are seeing ads for products and services they may be interested in. Doing this has already increased return on ad spend across US Amazon DSP campaigns by over a third 4. This further evidences how we can solve for the future of addressability without relying on third-party cookies or other ad identifiers.

Empowering brands with clean rooms

Clean rooms are central to giving marketers durable analytical capabilities in a world without ad identifiers. Why? Because they’re privacy-safe spaces that enable brands to perform queries across the pseudonymous signals that are available to them. Crucially, this helps marketers to understand how they are reaching customers across different channels, as well as how their ads across those channels are (or aren’t) delivering business impact.

It’s important to remember however that while clean rooms have the potential to empower brands, they are reliant on the inputs they receive. By collaborating across first-party signals and third-party inputs in a clean room, marketers can perform analytics to help them understand customer shopping journeys, generate unique audience segments, and analyse ROI in a safe and secure way.

For example, one domestic appliance brand utilised Amazon Marketing Cloud (AMC), the Amazon Ads clean room solution, to improve the efficiency of their ad spend. The brand worked with their agency, Kepler, and tapped into the Kepler Intelligence Platform (KIP) dashboard that makes AMC analysis available in real time to identify emerging trends, enabling them to see when customers were most likely to engage with their adverts. They found that while early mornings saw far less efficient conversions, the same activity was far more likely to engage audiences later in the day. With this insight, the brand implemented dayparting to ensure that ads were only displayed at those more active times. This change resulted in a 46% increase in orders, 66% increase in sales and a 15% increase in ROI 5.

The deprecation of third-party cookies offers brands the chance to do better and new technologies are already making this ambition a reality. Let’s take this opportunity now.

_____________________________________

1 Salesforce, WW, 2023

2 Source: Internal Amazon, U.S., Jan – Dec 2022, 140K campaigns across verticals

3 StatCounter, WW, 2022

4 Amazon Internal, US, 2023

5 Amazon Ads internal data, WW, 2023

This article was originally produced for New Digital Age.

In this week’s guest member blog post, we caught up with Søren H. Dinesen, the co-founder and CEO of Digiseg. Søren looks at sustainability, GDPR, first-party data and more to see if one-to-one marketing is realistically achievable. To find out more read below.

Our industry stubbornly clings to the promise of one-to-one marketing, convinced that it will deliver better results than advertisements that are designed to reach many. Complicating matters further, for the past six years we’ve struggled to achieve hyper-personalised targeting and simultaneously meet privacy regulations, but it isn’t working.

Cookies / Private Signals, Tomato /Tomahto

For reasons I can’t quite explain, our industry has reduced GDPR down to a restriction on cookies: Stop using third-party tracking cookies, the thinking goes, and compliance is more or less assured. But that’s following the letter rather than the spirit of the law.

At its core, GDPR says businesses need a legal basis to collect and use a citizen’s data; permission is one of eight bases. The industry is deploying technological workarounds -- replete with impressive mental gymnastics to convince ourselves that they are privacy compliant -- all so we can continue our quest for data-driven one-to-one marketing.

For instance, we collect user data of people who engage with our sites and apps. This is first-party data and that is fine. But then we work with other data companies that have vacuumed up vast troves of user data to create User ID graphs so that we can match users who visited our site to their mobiles, work computers, smart TVs in the family rec room or hashed emails. Who needs tracking cookies?

Or, we’ll take the data we’ve collected, and enter into a data clean room with a partner so we can compare and contrast data for marketing purposes. This tactic assumes that GDPR doesn’t require us to get the citizen’s permission prior to using their data in a clean room in order to develop a joint customer list for a promotion. That assumption is questionable.

But if we’re being honest with ourselves, we must ask: Do such use cases serve humanity’s request for privacy? Or are we acting in ways that will inevitably prompt another round of consumer blowback and regulations?

And while we’re on the topic of honesty, let’s talk about the efficacy of all that invasive one-to-one targeting. Does it really deliver significantly better results?

The Truth About One-to-One Marketing

Prior to joining Digiseg I led the marketing team of a company keen to acquire new customers. I was under intense pressure to tie every Euro I spent back to a customer. We struggled to grow our customer base and finally, out of desperation, I asked for and received money to launch a TV campaign. Guess what? In two months we doubled our customer base.

This isn’t an anti-digital advertising screed. I am a huge fan of digital advertising, and I work for a company that’s in the business of providing data to marketers and agencies so that they can execute and measure both performance and branding campaigns. We just don’t buy into the notion that success can only be achieved via one-to-one marketing.

The truth is, privacy and performance are not mutually exclusive terms. We don’t need to find new cookie-like ways to build awareness and acquire new customers.

Forget Consumers: Think Household Cohorts

A key to complying with the spirit as well as the letter of the privacy laws -- and to avoid incurring the citizen’s wrath once again -- is to improve on the one-to-many strategy. This, in turn, requires us to replace private signals (e.g. hashed emails, device IDs) with household cohorts.

Household cohorts are segments of users built on data from national statistics offices, such as the building–, motor-, tax- register or census data. The data provided by these civic sources are verified, scrubbed of all PII data, and very rich. For these reasons, it is often an advantage in scenarios where hyper-targeting results in diminishing returns by continually targeting the same subset of consumers.

For instance, household cohorts encompass insights such as home type, savings level, education level, presence of children, lifecycle, number of cars, neighbourhood type and tech level. It also provides insights into preferences, such as propensity to travel.

The benefit of these data types is they do a better job in validating a need for a product than audience segments based on tracking cookies. Plenty of people read about advancements in solar panels, but if they rent apartments in high-rise buildings, they’ll never buy one. But a neighbourhood filled with single family homes in a jurisdiction that offers tax incentives for renewables is a great audience segment? That’s a perfect target to drive conversions.

Put another way, these data allow marketers to reach the entire market, and across any channel, without ever tracking a single user. Instead, it drives conversions by targeting an entire market with the right messaging. Think of it as a data-driven strategy for one-to-many advertising, whether that’s a CTV campaign or a mobile one.

This one-to-many approach can apply to every task on the marketer’s to-do list, whether that’s targeting parents for a branding campaign, or driving users with a demonstrated need for your product to your website.

In these contexts, one-to-many advertising not only addresses the limitations of hyper-targeting but also leverages the strength of mass communication to build a stronger, more inclusive brand presence.

Google has signalled that the end of cookie-based targeting will arrive by the end of year. This is a good time for the industry to implement strategies that respect privacy, rather than pretend to. Let us hope that the deprecation of third-party cookies will usher in a new age, where one-to-many advertising allows us to engage with broader, less invasive advertising techniques that safeguard consumer privacy and still reach large audiences effectively.

Bio: Søren H. Dinesen is the co-founder and CEO of Digiseg. He began his career in the analog world, where he specialised in targeting and measurement in offline marketing. After successfully building and selling this data business, he shifted his focus to digital. In 2015, Dinesen founded Digiseg, seeing an opportunity to apply neighbourhood segmentation techniques to digital advertising. His goal was to develop a privacy-centric targeting and measurement technology that maintains high performance without the need for tracking.

In this week’s guest member blog post, we caught up with Iman Nahvi, Co-Founder, Chief Executive Officer at Advertima as he navigates the future of in-store Retail Media. To find out more read below.

The digital age has catalysed a transformative shift in Retail Media, primarily unfolding online and driven by real-time data analytics, audience targeting, and performance measurement, driving a monumental shift in advertising dollars toward retailers.

However, most shopping still occurs in-store, where the innovations of online Retail Media have not fully penetrated. Implementing digital screens without integrating key success factors such as real-time addressability, audience measurement, and data-driven performance analytics is insufficient. To revolutionise In-store Retail Media, a digital transformation involving advanced solutions is imperative to generate real-time audience data and replicate online success in brick-and-mortar contexts.

Traditionally, trade and shopper marketing funds are managed through direct deals between retailers and suppliers, necessitating precise planning and customisation. Programmatic platforms offer no advantages for these campaigns and lead to an inefficient outcome. Conversely, brand and media funds managed by media agencies require cross-channel access, making programmatic buying a suitable option. In-store retail media can align offers with audience-based solutions that meet the needs of existing brands to increase retail media revenue.

Programmatic DOOH (pDOOH) is effective for upper-funnel mass media but lacks real-time audience data integration. This gap extends to Digital Signage CMSs, which face latency issues incorporating such real-time data into bidding processes. Bridging this gap requires audience-based programmatic activation, integrating real-time audience data into bid streams to synchronise with ad displays, and enhancing efficiency and relevance.

Advertima uses advanced AI and predictive models to accurately predict audience presence and works with CMS platforms to ensure the integration of predictive insights into programmatic buying. Collaboration among CMS platforms, SSPs, DSPs, and retailers is crucial to embracing real-time audience segmentation and unlocking In-store Retail Media's potential.

Adopting audience-based programmatic activation is essential for achieving precision and effectiveness in-store, akin to online advertising. While challenges persist, embracing this approach promises to redefine the in-store shopping experience by merging retailer data richness with programmatic technology precision.

Read the full blog article here and learn how Advertima Audience AI can bring online capabilities to in-store.

Industry leaders from Diageo, Telecom Italia Mobile, Mail Metro Media, and RTL are among the first speakers to be announced for IAB Europe’s annual Digital Advertising and Marketing Conference, Interact in Milan on 21st and 22nd May.

IAB Europe has announced the first confirmed speakers for its annual flagship event Interact 2024. In partnership with IAB Italy, the latest edition of Interact will take place on the 21st - 22nd of May at Magna Pars in Milan, where leading European advertisers, industry experts, agencies & media owners will gather to tackle the industry’s most critical challenges and innovative opportunities head-on.

With a central theme of ‘The Big Questions. The Sharp Answers.’ speakers from Diageo, Telecom Italia Mobile (TIM), Mail Metro Media, RTL, Scope3, IAS, Samsung Ads, and many more will take to the stage to address and provide answers to the most pressing industry questions of today.

Join to hear from the following speakers and more:

The two-day conference will go beyond traditional keynote speeches and panel discussions with outstanding industry experts, brands, agency representatives, and publishers sharing their experiences, inspirations, and solutions to the industry’s biggest questions live on the Interact conference stage. From Ad Spend and AI to Retail Media, Privacy, Policy, Sustainability, and more each session on the agenda will focus on a thought-provoking question with answers being shared from the diverse speaker line-up.

Expect to gain answers to the following questions and more:

For more information on Interact 2024 and to view the first line-up of speakers, please visit the event website here.

Register now to secure your ticket!

Registration for the event is available here with early-bird discounted tickets available until 12th April. Tickets are selling quickly so secure your place today.